Publication of the FCA’s Business Plan for 2021/22 was delayed from its usual spot in April, finally appearing at the end of July. The document can be accessed here. An overview of the content follows.

Transformation

The plan contains a huge amount of mission/vision speak, as is typical in the annual reports of most large organisations. Much of the early space is devoted to highlighting successes and describing intended ‘transformation’ – how the FCA intends to operate more efficiently in future – investment in staff and technology and being more data driven being the key takeaways here.

There are sections on the wholesale markets and anti-fraud activities but probably of most interest to our readers is the section on retail consumer protection.

Retail consumers

The plan states that the FCA will:

- continue to deliver for consumers by taking forward the 4 priorities we identified in last year’s Business Plan, as well as our new Consumer Duty

- continue to enhance market integrity by reinforcing the effectiveness of UK wholesale markets and enhancing our supervisory approach to specific issues

- focus on 6 of the most important cross-market issues; fraud, financial resilience, operational resilience, improving diversity and inclusion, enabling a more sustainable financial future, and international cooperation

The first of these is a continuation of business as usual supervisory activities aimed at protecting consumers. The second implies higher level activity, no less important but not directly related to consumer facing activity.

The third bullet covers a lot of ground. Some might argue that elements included here are not the function of the FCA, for example the diversity and inclusion aspects. However, if the regulator intends, as seems clear, to involve itself in these matters then firms will need to have a weather eye on how they play within each business. The topic should at least be discussed at management body meetings and some level of formal or informal policy created.

International cooperation is to be expected as the FCA is widely accepted globally as a leading regulator. And, closer to home, the FCA continues to work with EU regulators to ensure that UK regulations dovetail with EU regulations where appropriate and diverge where it is believed that will be in the interests of the UK market. Based on various comments made by the FCA and others, it would not be a surprise if UK and EU regulations diverge more than merge over the coming years.

The plan outlines the FCA’s intentions in relation to encouraging and supporting ‘sustainable finance’ but ensuring that ESG focused products are marketed and managed correctly, for example by preventing greenwashing and similar misleading practices.

Everything else in the third bullet refers to specific concerns such as fraud and financial and operational resilience. It should be of some concern that, in relation to the latter two aspects, the FCA states:

“In line with our financial resilience survey, we continue to plan for a significant number of regulated firms, particularly smaller firms, to potentially fail in the year ahead, though recent economic data has been more encouraging.”

Retail Consumer Priorities

The four consumer priorities referred to are:

- enabling effective consumer investment decisions

- ensuring consumer credit markets work well

- making payments safe and accessible, and

- delivering fair value in a digital age

Consumer Duty

In addition, the FCA is making much of its proposed new Consumer Duty, which is currently under consultation. A summary and link to the consultation paper and online webinar can be found here.

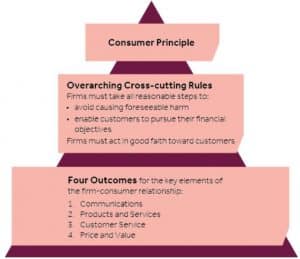

The proposed new duty on firms is intended to change or influence the culture within firms, in much the same way as the FCA Principles or TCF (remember that?). To that extent, the proposals are, in parts, a bit nebulous and vague. For example, firms are required to:

- act in good faith

- take all reasonable steps to avoid foreseeable harm to consumers

- take all reasonable steps to enable consumers to pursue their financial objectives

The graphic below is intended to show how the proposal will be structured.

The four outcomes are described as follows:

“We want firms to consistently place their customers’ interests at the centre of their business so that:

- communications equip consumers to make effective, timely and properly informed decisions about financial products and services

- products and services are specifically designed to meet consumers’ needs and sold to those whose needs they meet

- customer service meets the needs of consumers, enabling them to get the benefits of products and services and act in their interests without unnecessary barriers

- the price of products and services represents fair value for consumers”

Private Right of Action

However, there are some hints of real teeth being considered behind the consumer duty ‘fluffy stuff ‘– not least the regulator’s consideration of the potential merits and unintended consequences of introducing a private right of action (PROA) for breaches of the Principles, including any new Principle.

There are no actual proposals at this stage, the consultation paper simply exercises arguments for and against the introduction of a PROA and invites views. If implemented, the PROA would potentially open up a new avenue for consumers to obtain redress.

“We view a private right of action as part of a wider range of mechanisms through which firms are accountable for their breaches of our rules, and consumers can access redress. This includes firms’ own complaints and redress arrangements, the FCA’s supervisory and enforcement activities, access to redress through the Financial Ombudsman Service or redress schemes, and recourse to the Financial Services Compensation Scheme (FSCS).”

Fair value

The phrase ‘fair value’ is mentioned 12 times in the business plan. The charges levied at all stages in the investment and advice process, from fund manager charges to adviser charges have been a continuing focus for the FCA for a few years, increasingly so since the publication of the Asset Management Market Study in 2017. This study reached several conclusions, including that price competition in the investment market was weak. That led to a requirement for all funds to be assessed for ‘value’ at least annually. Read our recent article on this.

The frequent use of the concept of fair value in so many different sections of the business plan is a clue that the FCA continues to be driven by concerns over the effect of charges:

“Fees can have a dramatic impact on returns over time.”

The implication is that services at all stages in the investment/advice chain should be able to be delivered at ever lower costs through use of technology. The plan states:

“The new Consumer Duty will give firms more certainty about both our and consumers’ expectations of the standards they should meet.

- consumers can choose from products that meet their needs at a competitive quality and price

- digital innovation and competition support greater value for consumers

- consumers in vulnerable circumstances have fair access to key services and products, and firms do not exploit or target them with poor value products and services”

The business plan states that the outcome that the regulator wishes to see is that “the price of products and services represents fair value for consumers”. The related Consumer Duty paper CP21/13 clearly states that the FCA has no intention of acting as a price regulator then almost immediately warns that it might do just that if it is considered necessary in future:

“… we (do not) intend to use the proposed rule itself to introduce market

interventions such as price caps or other price interventions, for example, as we have done in the rent‑to‑own and overdrafts markets. In future we may need to use our regulatory tools to make such interventions where markets are failing to deliver fair value …”

All of which strongly suggests that charging models will come under close scrutiny. Firms need to be able to answer the question, “How do you satisfy yourself that your fees are fair value for your clients?”

Appointed Representatives (ARs)

Finally, it is worth mentioning that the plan refers to more targeted and tighter supervision of ARs and their principal firms. This is driven by problems that the regulator has seen in recent years from principal firms having poor due diligence and oversight of their ARs.

As part of this initiative, the FCA plans to consult on cross-sector changes to improve and strengthen elements of the AR regime later this year.

“Much of the AR regime is governed by FSMA. We will consider whether more fundamental changes are needed to the regime, including legislative change.”

A case of watch this space!

New Content Integration with Pacific Asset Management

Doug McFarlane Suitability 2025, Content Integration, content management, EU, FCA, Integration, Investment, ML, Pacific, Pacific Asset Management, PI, Update

We have some exciting news on the latest upgrade to ATEB Suitability on 9 April 2025. This update comes at no additional cost and provides a new addition to our content integration library. We have partnered with Pacific Asset Management to provide our customer firms with access to the following: A description of their service […]