The FCA has published policy statement PS21/6 – Implementation of Investment Firms Prudential Regime (IFPRU).

The policy statement alone fills 123 pages with an additional 237 pages of near final rules and form templates. By any measure this is a hefty document, and it is absolutely stuffed with jargon and snappy yet baffling new terminology such as:

- Prudential consolidation

- Proportional consolidation of participations

- SNI / non-SNI

- K-factor

- Consolidated K-AUM and K-CMH

- Non-K-conceNtration (the capitalised ‘N’ in the middle of the word seems a little unnecessary but there you go!)

In fact, there is so much of this stuff that an additional 23 pages are devoted purely to definitions! This is an important paper but not the easiest of reads.

But wait, there’s more! This PS is the response to CP20/24 (December 2020). CP 21/7 (April 2021) will lead to a second policy statement soon and a third consultation, expected to be published in Q3 2021 will result in a third policy statement and finalised rules. The intention is that the new rules will be effective from January 2022.

MIFIDPRU

The rules will reside in a brand new FCA sourcebook to be labelled ‘MIFIDPRU’. According to the FCA:

“The IFPR aims to streamline and simplify the prudential requirements for solo regulated investment firms in the UK (FCA investment firms) … it will shift the focus of prudential requirements and expectations away from risks that firms face, to also consider and seek to mitigate the potential for harm the firm can pose to consumers and markets. This includes consideration of the amount of own funds and liquid assets they should hold so that if a firm does have to wind down, it can do so in an orderly manner.”

Streamline and simplify are not the first two words that came to mind when reading the paper! But introducing the IFPR means that there will be a single prudential regime for all FCA investment firms, hence simplifying the current approach.

The rules will apply to:

- Any MiFID investment authorised and regulated by the FCA that is currently subject to any part of the Capital Requirements Directive (CRD) and the Capital Requirements Regulation (CRR) including:

- investment firms that are currently subject to BIPRU and GENPRU

- ‘full scope,’ ‘limited activity’ and ‘limited licence’ investment firms currently subject to IFPRU and CRR

- ‘local’ investment firms

- matched principal dealers

- specialist commodities derivatives investment firms that use the current exemption on capital requirements and large exposures including:

- oil market participants (OMPS)

- energy market participants (EMPS)

- exempt CAD-firms

- investment firms that would be exempt from MiFID under Article 3 but have ‘opted-in’ to MiFID

- Collective Portfolio Management Investment firms (CPMIs)

- regulated and unregulated holding companies of groups that contain an investment firm authorised and regulated by the FCA and that is currently authorised under MiFID and/or a CPMI.

The notable omission from this list is a firm that is optional Article 3 exempt. MIFIDPRU will only apply to firms that are currently authorised under the UK Markets in Financial Instruments Directive regime (MiFID). The scope of MiFID is not affected by MIFIDPRU. Firms that are not subject to MiFID, including those that are Article 3 exempt, are not affected by these proposals. Any firms which would be MiFID article 3 exempt but have previously opted-in to MiFID will need to apply for a variation of permission if they would like to stop opting-in.

Overview of MIFIDPRU

Although the PS includes near final rules, which the FCA expects will not be amended, there are two further consultation rounds to be factored in so we do not feel it is appropriate to go into great detail about the application of MIFIDPRU to different categories of firm. In any case, there are quite a few permutations so it would be ambitious, to say the least, to attempt to explain 237 pages of rules here. Instead, this article tries to summarise the main concepts so that in-scope firms will be able to make a start on identifying the preparation required.

The sourcebook will be created under these topic headings:

- Overview of MIFIDPRU

- Level of application of requirements

- Own funds

- Own funds requirements

- Concentration risk

- not defined

- not defined

- not defined

- Reporting

In addition, the introduction of MIFIDPRU necessitates some amendments to other sections of the FCA Handbook, not least TP, which will include details of transitional arrangements.

A new suite of 10 reporting forms will be implemented – 7 applying to all firms and 3 applying only to defined categories of firms (see below). All but 2 of the new forms will be required quarterly – the remaining 2 being annual reports. In case in-scope firms are already despairing at the thought of even more paperwork it is worth noting that all reporting will be done via Connect and the current COREP and FINREP reports plus 20 current FSA0xx forms will cease to be required.

Categorisation of investment firms

A key concept in the IFPR is that FCA investment firms will be categorised as either small and non-interconnected firms (SNI) or not (non-SNIs). Chapter 2 of the PS provides further clarification on:

- the firms that MIFIDPRU will apply to

- the scope of the IFPR and which firms will continue to be PRA-designated

- how/which MiFID activities determine a firm’s classification as SNI or non-SNI

- how thresholds impact a firm’s classification

Firms will have to self-determine whether they are SNI or non-SNI and they should monitor this. The FCA reckons that approximately 70% of firms to whom the IFPR applies will be SNIs. The categorisation is important as SNIs will have less stringent requirements to meet.

Firms should refer to MIFIDPRU TP 6 in the draft Handbook rules (in CP21/7) for information on how the FCA proposes that firms should determine their SNI status at the outset of the IFPR.

Once an FCA investment firm has been classified as a non-SNI, it must meet the requirements for being an SNI continuously for 6 months before it can be reclassified as an SNI. This is to prevent firms from moving between categories unnecessarily.

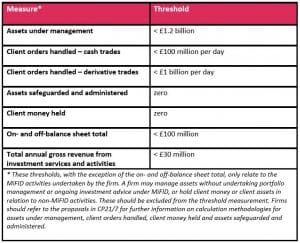

The quantitative criteria for categorisation as an SNI are shown in the table below.

New Content Integration with Pacific Asset Management

Doug McFarlane Suitability 2025, Content Integration, content management, EU, FCA, Integration, Investment, ML, Pacific, Pacific Asset Management, PI, Update

We have some exciting news on the latest upgrade to ATEB Suitability on 9 April 2025. This update comes at no additional cost and provides a new addition to our content integration library. We have partnered with Pacific Asset Management to provide our customer firms with access to the following: A description of their service […]