In our article last week, we highlighted the deadlines for implementation of Consumer Duty – 30 April and 31 July …

… the rules for existing products and services take effect on 31 July and the earlier deadline of 30 April is for Manufacturers to have completed some preparatory work.

Hard on the heels of that article, came news of a survey that Aviva had conducted with 1003 advisers, The trade press headlines were as usual, eye-catching …

“59% of advisers haven’t started consumer duty preparations”

… but, also as usual, not quite reflective of the actual situation.

First, the survey was carried out in February so that was at least a month ago and possibly close to two months. Many firms may have geared up in the interim and started work on Consumer Duty.

Second, the headline figure implies that a majority of firms have pretty much ignored the whole thing. The underlying details paint a less dramatic picture in that, according to the survey, 41% have already started work and, of the remaining 59%:

- 26% said they are clear on how they will prepare but have not started yet

- 16% said they do not know how they will prepare and have not begun

- 17% said they have no concerns

The 26% are clearly on the case but simply had not commenced work as at February 2023 – it is surely reasonable to presume that at least some of those now have started.

The 16% is more of a potential concern but it clearly comprises firms that are a) aware of the imminent requirement to do something and b) will presumably seek appropriate assistance – perhaps from ATEB!

So, the true picture would appear to be that only 17% indicated that they believe they have it all sorted already. This group possibly presents an even bigger concern. Some of these firms may well ‘have it all sorted’, either because they started preparations months ago or because the firm’s business model and processes were already in good shape. But it is almost inevitable that some will be in a state of denial or believe, without foundation, that their business model is perfect.

APRIL …

Anyway, back to the deadlines. It could be that firms are simply seeing just the July deadline because they are ‘only distributors’, defined in the rules as:

“firms that offer, sell, recommend, advise on, propose or provide a product or service”

But this assumption would be to ignore the fact that many, if not most, firms will also be manufacturers. The FCA sent a Dear CEO letter to firms on 30 January, stating:

“Under the Duty, firms can be manufacturers of services as well as products. So, for example where a wealth management firm offers discretionary management services, they would be a manufacturer of that service.”

“We often see distributors working with other firms to co-manufacture products and services: e.g., bespoke Discretionary Managed Portfolio Services / fund ranges and white-labelled platforms. Where this is the case, the firms are likely to be classed as co-manufacturers and would need to have a written agreement setting out their respective roles and responsibilities under the rules.”

The key here is to stop thinking about a ‘product’ in its traditional sense and recognise that Consumer Duty covers both products AND services. Product is defined as:

“any specified investment distributed or to be distributed to retail customers; and any service which involves or includes the carrying on of a regulated activity or an ancillary activity … which is provided directly to a retail customer”

So, firms need to consider whether they are in any sense operating services (or even products) that would qualify them as a manufacturer. If so, the 30 April deadline applies and is the date by which manufacturers should have completed all the reviews necessary to meet the outcome rules for their existing open products and services.

Could you be a manufacturer?

In many cases, the answer will be a resounding, if surprising, ‘YES’!

The definition of a manufacturer is a firm that:

“creates, develops, designs, issues, manages, operates, carries out, or (for insurance or credit purposes only) underwrites a product”

In assessing whether this applies, firms must identify whether and to what extent they influence the features of the product or service. Having considered this aspect in depth, we list below some activities that adviser firms are likely to be involved in and which could carry a manufacturer or co-manufacturer status. The common factor in each of these is that the firm is a manufacturer (or co-manufacturer) wherever the firm can determine or materially influence the manufacture of a product or service. This would include a firm that can determine the essential features and main elements of a product or service, including its target market and price.

Activities/services that might constitute manufacturing include:

- Running a model portfolio

Degree of certainty – 100%

A firm that has a decision-making role on elements such as the target market or investment strategy, would be regarded as a co-manufacturer under the products and services outcome and the price and value outcome. - Ongoing review service

Degree of certainty – 100%

Firms may not immediately recognise this as a service of which they are the manufacturer, but it is clearly the case. Most advisory firms operate an ongoing review service. Indeed, ongoing reviews are usually a default part of being invested in the firm’s CIP. It is the firm that decides what the service looks like, frequency / cost / charges etc. The service did not fall fully formed from the sky. Someone had to create it, manufacture it if you will, – and that was the firm! This is confirmed in the Finalised Guidance from July 2022.“The financial adviser: The firm must consider how it meets the Duty in the design and delivery of its initial and ongoing advisory services …”. The firm’s obligations include:- Considering the needs of the target market.

- Following the consumer understanding rules for its communications.

- Considering if its charges provide fair value.

- Considering the overall outcomes being delivered for the customer, including whether the overall cost to the customer, including all product and distribution charges in the distribution chain, provides fair value. In our view, this would have to include appropriate consideration of whether each client needs ongoing reviews or whether an ‘advice on demand’ relationship would be as, or more, appropriate and cost effective for the client. See our recent article on this topic.

- Considering if the customer is given an appropriate level of information about the overall proposition, in a timely and understandable format, to enable the customer to make effective decisions.

Note that these are ongoing obligations, not just a one-off for 30 April.

- Creating and running a financial instrument

Degree of certainty – 100%

We know of adviser firms that have set up their own OEICs or other instruments. They clearly fall into the manufacturer camp in respect of those products. - Bespoke service for an individual client

Degree of certainty – 100%

In general, the rules apply at the level of the target market, rather than a firm’s services for an individual customer. So, firms need to review the service at that level, rather than for each customer. These rules would only apply at an individual customer level where a bespoke service is developed for a particular customer. - Discretionary portfolios – the DIM/DFM

Degree of certainty – 100% (for firms that provide the portfolio management service)

It is obvious that the firm providing the discretionary management service has to be a manufacturer. And the Duty imposes new obligations on firms acting under the ‘agent as client’ rules in COBS 2.4.

Firms must consider if there are retail customers at the end of the distribution chain and if they can determine or materially influence outcomes for them. Where this is the case, firms must comply with the Duty. For example, when developing a target market, ensuring products or services are designed to meet their needs and objectives, or assessing value for a product or service, a firm needs to consider the end retail customers in the distribution chain, even if it does not have a direct customer relationship with them. - Discretionary portfolios – the adviser firm

Degree of certainty – varies according to the exact nature of the firm’s involvement

It is less obvious, but entirely possible, that there may be some activity undertaken by the adviser firm that constitutes manufacturing. Firms need to assess the process of using a DFM/DIM portfolio for clients against the criteria of ability to determine features of the service.

We believe that most discretionary portfolios are still operating on an ‘agent as client’ basis. This model is convenient for the portfolio manager but comes with many downsides for the advising firm and even more for the end client. We have written at length about this previously, see here.

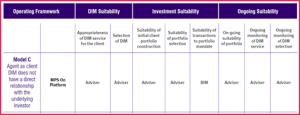

Is ‘acting as agent’ a service that you are providing to clients? If so, it needs to be considered under the manufacturer outcomes. And before readers conclude that they do not have sufficient involvement to warrant consideration of whether ‘manufacturer’ applies just look at the table below (Source: PFS Good Practice Guide Addendum/May 2017) which indicates the one aspect that the DIM does and the seven aspects for which the adviser is responsible! Even if manufacturing is considered not to apply, firms still carry distributor obligations. And it is not easy to see how the downsides for the client of the agent as client arrangement can be squared with those obligations.

Even if manufacturing is considered not to apply, firms still carry distributor obligations. And it is not easy to see how the downsides for the client of the agent as client arrangement can be squared with those obligations.

Why is this all so difficult?

You might well ask! Why did the FCA simply not provide clear definitions and examples of a ‘manufacturer’ and ‘distributor’? The FCA addressed this question in the finalised guidance paper, stating:

“Where relevant, these terms include activities under the Financial Services and Markets Act 2000 (Regulated Activities) Order 2001 in relation to retail market business. For example, managing includes ‘managing investments’ …

However, the terms are not limited to specific definitions and firms should look to the plain language meaning. The concepts are deliberately broad, and the terms may overlap, to capture all aspects of the design, launch and ongoing operation throughout a product or service’s life.

The rules apply to the manufacture of products and services. Services include those involved in carrying on a regulated activity or activities connected to providing a payment service or issuing electronic money.

This covers all services including, for example, a distributor’s sales processes, operating an investment platform, operating a model portfolio service, debt counselling services and arranging transactions.”

The FCA considers, correctly in our view, that there are too many variations and permutations of activities that might constitute manufacturing, distributing or both. The only solution is for each firm to undertake and document consideration of the exact nature of its activities in concluding which Duty obligations apply.

New Content Integration with Pacific Asset Management

Doug McFarlane Suitability 2025, Content Integration, content management, EU, FCA, Integration, Investment, ML, Pacific, Pacific Asset Management, PI, Update

We have some exciting news on the latest upgrade to ATEB Suitability on 9 April 2025. This update comes at no additional cost and provides a new addition to our content integration library. We have partnered with Pacific Asset Management to provide our customer firms with access to the following: A description of their service […]